Many milestones have been recently achieved in a relatively short time, thanks to digital solutions that have exacerbated financial inclusion. Today, the wave of technological innovations and ongoing Internet growth has fundamentally reshaped the banking industry, creating tremendous new opportunities.

At the heart of the transformation lies the dynamic and multifaceted concept of inclusion, with financial inclusion standing as its core aspect. Sustainable progress in this realm necessitates the integration of digital and innovative banking solutions, ensuring that financial services cater to the needs of all, including the most vulnerable segments of society.

According to the African Digital Banking Transformation 2023 report, banking access increased exponentially from 24% in 2017 to 48% in 2022 in Africa [1]. This expansion has not only broadened the scope of banking practices but has also provided policymakers with a wider array of options to make financial services more accessible, particularly to the continent’s unbanked population.

Besides, it has empowered marginalized groups with equal access to high-quality financial services. Fostering innovation has proven instrumental in enhancing financial access for small and medium-sized enterprises, including women-led ventures. By leveraging digital banking tools and solutions, barriers to financial inclusion are gradually being dismantled, creating room for more inclusive economic growth and development across Africa.

Account for Young Generation

Increased adoption of banking innovations has facilitated access to financial services in areas that traditionally lacked banking networks. An estimated 48% of the African population has access to banking services today. This growth has been associated with the trend of embracing digital banking solutions. Although financial transactions in Africa are still dominated by cash, representing approximately 90%, digital and electronic solutions account for 5% to 7% [1]. This indicates a major potential for further growth in the digital banking sector to foster the inclusion of the emerging younger generation. The younger population provides a ready market for inclusion in the digital banking solution.

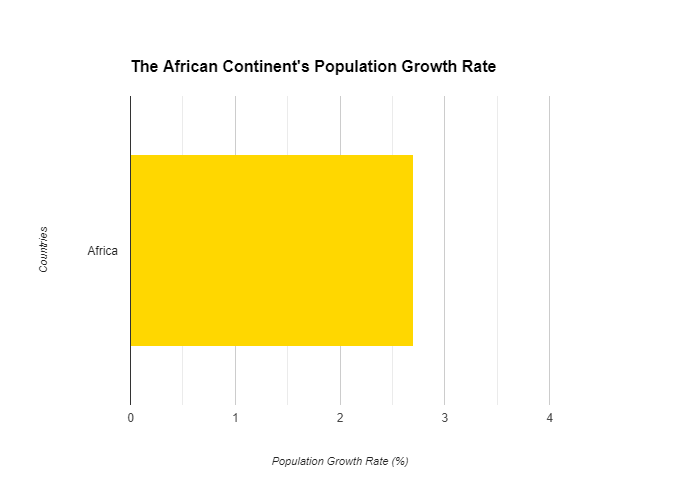

The African continent features one of the fastest population growth rates worldwide, averaging 2.7% per year, compared to an estimated global average of 1%, with a median age of 20 years [2]. Africa is witnessing a surge in a new generation of younger and urban consumers inclined to embrace digital technologies due to their convenience in facilitating online transactions.

Africa’s young population, characterized as the most significant smartphone users with a heavy online presence, has created an ideal environment that favors the rapid adoption of digital banking solutions across the African continent. In this domain, digital banking solutions favor the inclusion of younger generations to cater to their financial needs and preferences.

Inclusion of Marginalized and Underserved Populations

Marginalized and underserved populations in rural demographic settings are the biggest drivers of digital banking because the traditional delivery of financial services in these areas i

s less available. With significant technological innovations and integration, the digitalization of banking services has improved connectivity across the banking and financial industry and changed the way services are delivered to excluded populations. Digital banking solutions in Africa have contributed significantly to a paradigm shift towards branchless banking services, improving financial inclusion. The growing penetration of digital banking, combined with Internet access via mobile devices, has favorably transformed consumer behavior in rural African areas, as going online becomes an essential aspect of people’s daily lives.

Unlike the traditional approach to banking that was marketed by banking infrastructure shortcomings to create a barrier for marginalized populations, digital banking overcomes these gaps to promote the financial inclusion of marginalized populations in Africa. Individuals in rural areas across African countries now prefer to check their financial balance via smartphones rather than moving hundreds of miles away to visit ATMs or bank branches. This increased access to bank services via technological innovations among underserved populations helps in reducing the financial infrastructure gap, where the cost of distance and time pose constraints for rural populations.

ATM Density in North Africa by Countries | Source: Statista

According to McKinsey’s survey of digital solutions in Africa, some notable countries that have managed the transition to digital innovations for delivering complex electronic payment systems include Egypt, Kenya, Ghana, Nigeria, and South Africa. For instance, digital wallets linked to different payment methods, including accounts, mobile money, and cards, have grown in availability and adoption as digital banking solutions catering to the underserved and marginalized population [2]. Similarly, digital banking solutions that enable easier and more convenient consumer transactions have been integrated to facilitate inclusion. For example, integrated universal QR codes developed or sponsored by central banks or regulatory institutions are helping minimize payment method complexities.

In Ghana, Ghana Quick Response (GHQR) enables the synchronization of payment between bank accounts, cards, and mobile money. Similarly, NQR is a similar solution offered in Nigeria. In the sub-Saharan region, Kenya has been a pioneer in mobile wallet transactions, accounting for up to 87% of its GDP in 2021. Kenya has also demonstrated an increase in access to banking services from 26% to 83% from 2006 to 2021, respectively [3].

Addressing Gender Gaps

Gender equality is not only an important right but also a core indicator of prosperity in the modern financial service industry. Addressing gender gaps is a crucial factor in facilitating financial access. Digital banking solutions favor financial inclusion in Africa by closing the gender gap in accessing financial services. According to the International Monetary Fund’s report on women’s access to financial services, only 37% of women had bank accounts compared to 48% of men in sub-Saharan Africa [4].

The statistics were worse in North African countries, where an estimated two-thirds of the population had no bank accounts, while the gender gap stood at 18% [4]. Despite the gender gaps, today’s digital transformation in the banking sector provides new avenues for the financial empowerment of women.

Digital banking solutions are critical in achieving the goal of women’s inclusion in financial services. They support women’s participation in the financial market, increase their financial autonomy, and enhance the performance of their businesses through expanded access to financial services. Digital banking can be attributed as a viable solution to narrowing the gender gap in bank account ownership and fostering formal financial activity in terms of volume and value transactions.

This technological environment is favorable in promoting affordable, transparent, reliable, and accessible banking services for women. With this, women can formally save and increase their formal participation in the financial market.

It is worth noting the contribution of digital banking solutions in improving the performance of small and medium-sized businesses owned by women entrepreneurs. At the top of the challenges faced by SMEs in most emerging African markets is a critical need for access to finance to realize their potential growth. This issue is particularly real in SMEs owned by women due to local financial conditions related to inadequate financial structure or a lack of collateral for securing credit. The financial footprints associated with digital transactions or payments have made it possible for banks to assess the creditworthiness of women without traditional credit assets. This has allowed women expanded access to credit and insurance, which can support women-owned businesses.

In Ethiopia, the Women Entrepreneurship Development Project (WEDP) was established as an IDA operation giving loans and entrepreneurship training to women-owned SMEs. WEDP was rolled out as a microfinance institution after identifying financial gaps linked to a lack of individual-liable loans for women entrepreneurs. WEDP loan led to over 40% annual profits increase, 56% of net employment for Ethiopian women entrepreneurs, and training of over 20000 female entrepreneurs [5].

Conclusion

In conclusion, Africa is at a turning point. The advancement of digital banking solutions in African countries marks a transformative era in terms of fostering financial inclusion across the continent. The remarkable increase in banking access, especially among marginalized populations and the younger generation, underscores the pivotal role of digital innovations in reshaping the financial landscape. Through the integration of digital technologies, banking services have become more accessible, convenient, and tailored to meet the diverse needs of individuals and businesses, thereby bridging the gap of financial exclusion. Moreover, the focus on addressing gender disparities in accessing financial services highlights the significant strides made through digital banking solutions. By providing avenues for women to participate in the formal financial market and empowering them with access to credit and resources, digital banking has become instrumental in enhancing women’s financial autonomy and fostering entrepreneurship. The success stories of initiatives like the Women Entrepreneurship Development Project in Ethiopia demonstrate the tangible impact of digital banking solutions in driving economic growth and empowering women-owned businesses.

References

- African Digital Banking Transformation Report 2023

- The Future of Payments in Africa

- African Banks Progress towards Digitalisation

- Access to Finance: Why Aren’t Women Leaning In?

- Small and Medium Enterprises (SMEs) Finance